Notes receivable accounting

Content

Notes Receivable are an asset as they record the value that a business is owed in promissory notes. A closely related topic is that of accounts receivable vs. accounts payable. Notes receivable are a balance sheet item that records the value of promissory notes that a business is owed and should receive payment for. A written promissory note gives the holder, or bearer, the right to receive the amount outlined in the legal agreement. Promissory notes are a written promise to pay cash to another party on or before a specified future date. Notes receivable are generally considered to be an asset on a company’s balance sheet.

- If the amount of notes receivable is significant, a company should establish a separate allowance for bad debts account for notes receivable.

- Notes receivable contain a debit balance that will increase in amount when debited and reduce when credited.

- Notes receivable is a term used in accounting to describe any written promise of payment from a customer or client.

- When the maker of a promissory note fails to pay, the note is said to be dishonored.

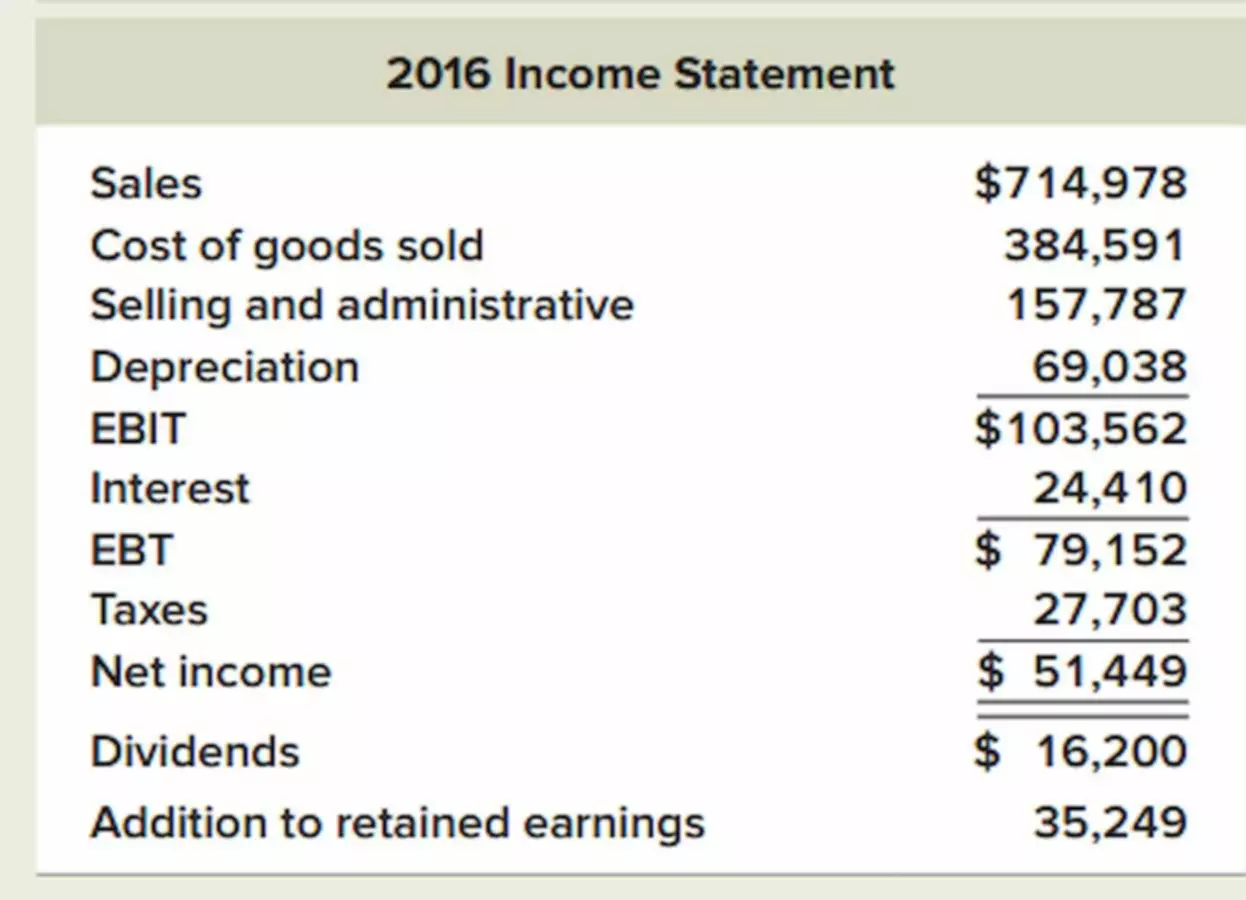

Yummy Foods did this in good faith and because it has a good relationship with the supplier. This is, however, the first time that the company has had to deal with a Note Receivable. You are in charge of preparing the balance sheet for the 2019 fiscal year. The interest earned on the note by Company A every month would be recorded on Company A’s income statement as interest revenue.

What are the benefits of notes receivable?

If interest on a bad debt had previously been accrued, then a correcting entry is needed to remove the accrued interest from interest revenue and interest receivable . The amount of credit sales is multiplied by the percentage that management estimates is uncollectible. Factors to consider when determining the percentage amount to use will be trends resulting from amounts of uncollectible accounts in proportion notes receivable to credit sales experienced in the past. The resulting amount is credited to the AFDA account and debited to bad debt expense. Note how another contra account, the sales returns and allowances account, is used to record the debit entry for the previous two journal entries above. Its purpose is to track returns and allowances transactions separately, as opposed to directly recording them as a debit to sales.

This is because not all the sales made to a particular customer are recorded in the customer’s subsidiary accounts receivable ledger. There are several types of notes receivable that arise from different economic transactions. For example, trade notes receivable result from written obligations by a firm’s customers.

What Is a Note Receivable?

This is a fast and simple way to estimate bad debt expense because the amount of sales is known and readily available. This method also illustrates proper matching of expenses with revenues earned over that reporting period. Remember, just use credit sales, watch for any indication of cash sales. When accounts receivables exist, some amounts of uncollectible receivables are inevitable due to credit risk.

Below is the schedule for the interest and amortization calculations using the effective interest method. Below are some examples with journal entries involving various stated rates compared to market rates. All financial assets are to be measured initially at their fair value which is calculated as the present value amount of future cash receipts. This section of the chapter is intended to be a summary overview of the methods and entries used to estimate and write-off uncollectible accounts originally covered in detail in the introductory accounting course.

Set your financial reporting on autopilot. Goodbye manual work.

Our writing and editorial staff are a team of experts holding advanced financial designations and have written for most major financial media publications. Our work has been directly cited by organizations including Entrepreneur, Business Insider, Investopedia, Forbes, CNBC, and many others. Finance Strategists is a leading financial literacy non-profit organization priding itself on providing accurate and reliable financial information to millions of readers each year. At Finance Strategists, we partner with financial experts to ensure the accuracy of our financial content. The articles and research support materials available on this site are educational and are not intended to be investment or tax advice.

- Therefore, when payment is made on a note receivable, both the balance sheet and the income statement are affected.

- The $18,675 paid by Price to Cooper is called the maturity value of the note.

- A note can be requested or extended in exchange for products and services or in exchange for cash .

- If a note is issued on the last day of a month and the month of maturity has fewer days than the month of issuance, the note matures on the last day of the month of maturity.

- The individual or business that signs the note is referred to as the maker of the note.

- Accrued assets are assets, such as interest receivable or accounts receivable, that have not been recorded by the end of an accounting period.

- Notes receivable include principal and interest, and short-term and long-term notes receivable have the same interest calculation.

This ensures that there is a specified timeline for receiving payments, which makes it easier for businesses to plan their cash flows. As a business owner, you may have heard of the term “notes receivable” floating around in financial discussions. Simply put, notes receivable refers to any written promise of payment that a customer or client owes to your business. As with any asset, notes receivable can greatly benefit your business’s financial standing if managed properly.

Key Components of Notes Receivable

Companies purchasing goods and services that do not take advantage of the sales dis- counts are usually not using their cash as effectively as they could. For example, a purchaser who fails to take the 1.5% reduction offered for payment within ten days for an account due in thirty days is equivalent to missing a stated annual interest rate return on their cash for 27.38% (365 days ÷ 20 days × 1.5%). For this reason, companies usually pay within the discount period unless their available cash is insufficient to take advantage of the opportunity. To record a note receivable, you will need to debit the cash account and credit the notes receivable account. Notes Receivable are financial instruments that represent a promise of payment from a debtor to the creditor. When a company lends money to another entity and expects repayment within one year or less, the loan is classified as a current asset on the balance sheet.